367 GW by 2032. Where the hell is it all coming from?

ERCOT just filed a forecast projecting a 4x increase in Texas peak power demand by 2032. The number is probably wrong. The crisis underneath it is not. Three questions nobody in the hype cycle wants to answer — with the data to back them up.

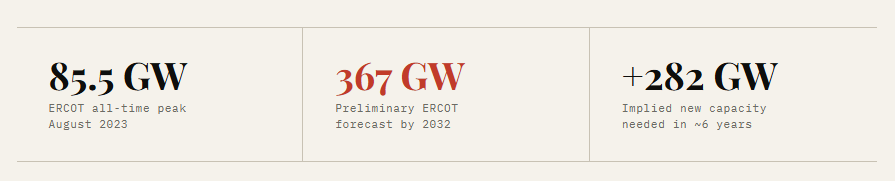

ERCOT filed a preliminary long-term load forecast last week projecting 367,790 MW of peak demand by 2032 — more than four times the current all-time record. The filing immediately went viral across energy Twitter, LinkedIn, and every utility trade publication on the internet.

Most of the commentary missed the point. The debate about whether 367 GW is real is mostly theater. ERCOT's own senior vice president filed comments the same day asking the PUCT not to use the number for any reliability or resource adequacy analysis. Strip out the speculative pipeline and the base case lands around 111 GW — still a 30% increase over today's record, still an unprecedented build challenge, and still something the current equipment and workforce supply chain cannot meet on any credible timeline.

So let's ask the three questions that actually matter.

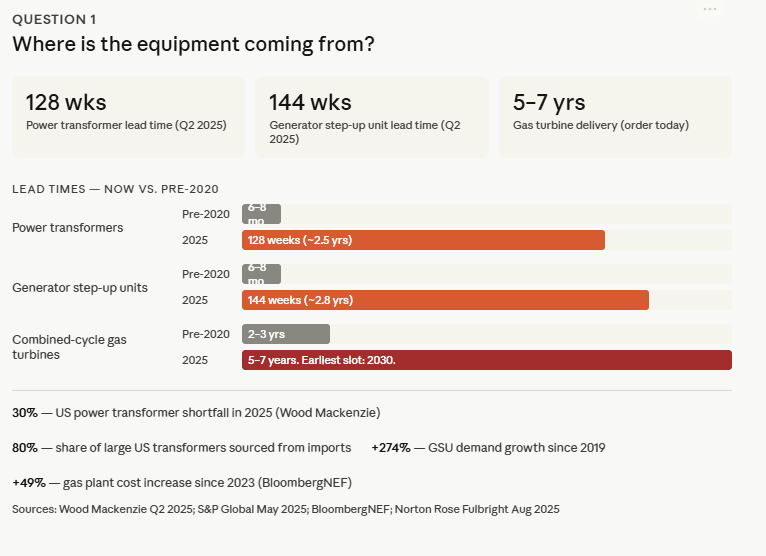

Question 01: Where is the power equipment coming from?

You cannot build generation or transmission without transformers and turbines. Both are in a supply crisis that no headline forecast changes.

Power transformers — the equipment that makes transmission possible — are averaging 128-week lead times as of Q2 2025. Generator step-up units (GSUs), required for every utility-scale generation project, are at 144 weeks. That's nearly three years to get the basic equipment before you break ground. And domestic manufacturing covers only about 20% of US demand — the rest relies on imports that are now themselves constrained by global competition and raw material shortages.

Gas turbines are worse. If you order today, the earliest realistic delivery slot for a large combined-cycle turbine is 2030. There are only three major vendors globally — GE Vernova, Siemens Energy, Mitsubishi Power. Around 120 to 130 advanced-class units are available annually worldwide. When Saudi Arabia ordered roughly 30 turbines in one transaction, that consumed nearly a quarter of global annual supply.

"Frankly, we can't make enough gas turbines to support this market. What a difference a few years make."

— Siemens Energy North America President, POWERGEN International 2025

The equipment math doesn't get better just because the demand forecast is dramatic. Copper prices are up over 70% since 2020. Grain-oriented electrical steel — the core material in every power transformer — has one domestic US producer. The tariff environment has made imports more expensive, not more available. This is not a financing problem. It's a manufacturing and physics problem.

Sources: Wood Mackenzie Q2 2025 · S&P Global May 2025 · BloombergNEF Feb 2026 · Norton Rose Fulbright Aug 2025

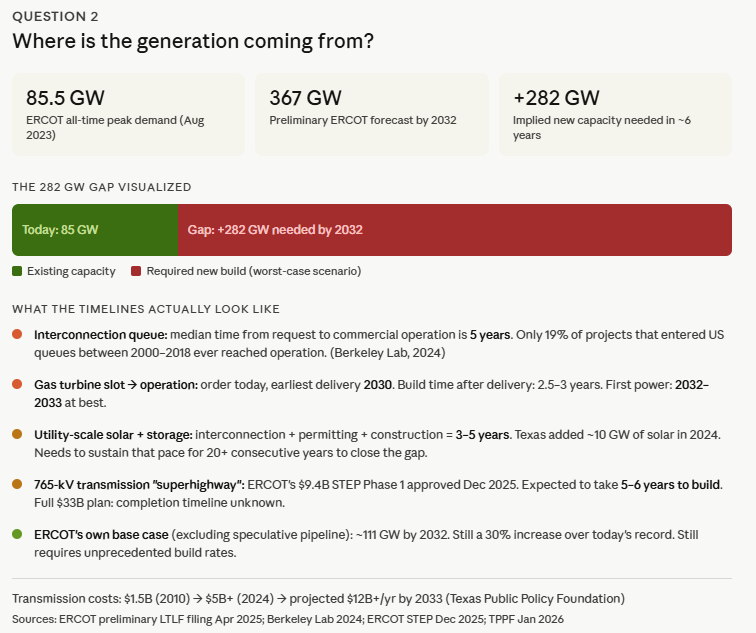

Question 02: Where is the generation actually coming from?

ERCOT received 2,000 new generation interconnection requests in 2025, totaling 432 GW. Solar and storage account for 77% of that. It sounds like a lot. The timelines tell a different story.

The large-load interconnection queue is itself part of the problem. ERCOT is now tracking approximately 410 GW of large loads seeking interconnection, of which 87% are data centers. Data center load alone accounts for 228 GW of the submitted large-load requests by 2032. Oncor's territory goes from roughly 5 GW in large-load submissions in 2026 to over 109 GW by 2032 — if everything that's been submitted actually shows up.

It won't. But even the fraction that does will require a pace of grid buildout that has no historical precedent in the US power sector. Transmission costs in ERCOT have already gone from $1.5 billion in 2010 to over $5 billion in 2024. They could exceed $12 billion per year by 2033. That cost lands on ratepayers unless the regulatory framework changes — and that fight is already starting.

Sources: ERCOT Preliminary LTLF Filing Apr 2026 · Berkeley Lab 2024 · ERCOT STEP Approval Dec 2025 · Texas Public Policy Foundation Jan 2026

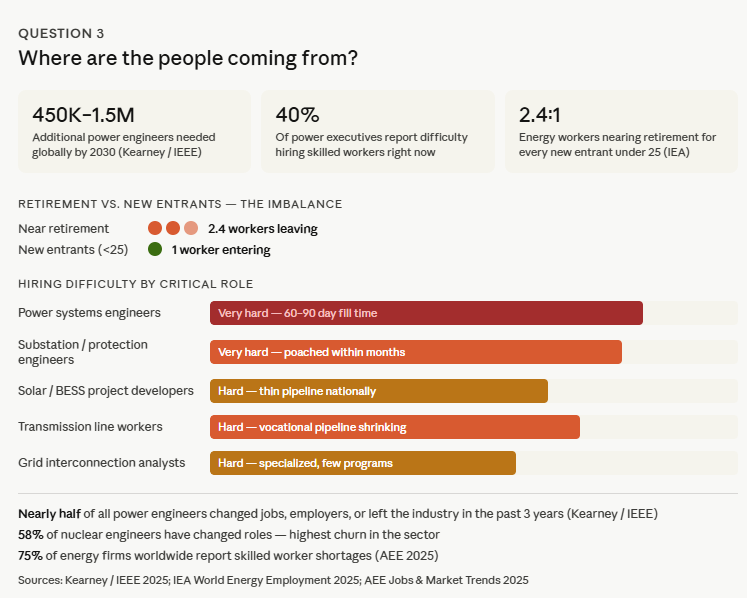

Question 03: Where are the people coming from?

This is the one everyone ignores. You cannot build 282 GW — or 30 GW — without the engineers, project developers, and construction workforce to design, permit, and build it. That pipeline is thinning faster than any interconnection queue is filling up.

The workforce gap:

Structural imbalance: 2.4 workers are nearing retirement for every 1 new entrant under 25. Nearly half of all power engineers changed jobs, left their employer, or left the industry entirely in the past 3 years.

The companies building critical energy infrastructure are now competing not just with each other for engineers and project developers — they're competing with tech, defense, semiconductor, and EV manufacturing sectors, all of which are expanding simultaneously and drawing from the same shrinking pool of applied technical talent.

"Without enough engineers, these critical projects will be delayed, compounding reliability risks and slowing the energy transition at the exact moment when momentum is needed most."

— André Begosso, Kearney (Kearney / IEEE Power Engineering Study, 2025)

The workforce math compounds the equipment math. You need engineers to design the projects. You need project developers to move them through interconnection. You need construction workers to build them. You need grid operators to run them. Every one of those pipelines is constrained. And unlike equipment lead times, you cannot solve a workforce shortage by placing a large order two years in advance.

Sources: Kearney / IEEE Power Engineering Workforce Study 2025 · IEA World Energy Employment 2025 · AEE Jobs & Market Trends 2025

So what actually happens?

The 367 GW number will get revised. ERCOT said so themselves the day they filed it. But the direction of travel is not in question.

Texas is adding large load faster than any grid in the country has ever had to absorb. The infrastructure buildout required to meet even a fraction of that demand — three-year transformer queues, five-to-seven-year gas turbine backlogs, five-year average interconnection timelines, a workforce aging out faster than it's being replaced — is the largest capital deployment challenge in the ERCOT region in a generation.

The companies winning in this environment aren't the ones chasing the 367 GW headline. They're the ones who ordered equipment two years ago, locked interconnection positions before the queue exploded, and are building the technical teams now to execute when the permits clear. The ones that wait will be bidding $50K over market for engineers who already have three offers.

That last part is where I work.

Do you think the math works — or does this end in rationing?

———

root/edge — Executive & senior technical search · Energy transition & power infrastructure

Lars Gloessner